Greek'ler ve Örtük Oynaklık

As the option price does not always appear to move in conjunction with the price of the underlying asset, it is important to understand which factors contribute to the movement in the price of an option and what effect they have. Using theoretical prices and implied rates dxPrice engine derives Delta, Gamma, Vega, Theta, and Rho that allow our users to get more deep insights on the reasons for option price changes.

Implied volatility shows the volatility of an underlying asset expected by options traders. The dxPrice engine calculates the value and provides it to our users in an easily accessible manner.

Unlike all other indicators, Greeks and Implied Volatility are derived using the analytical formulas of the Black-Scholes model. Model-free price and implied rates are used as input parameters to the model.

Series and Underlying level Analytics

The Series and Underlying records are distributed in the feed and provide users with some analytical indicators calculated for options series and/or chains (underlying group). A simple demo UI for the dxPrice results can be found here.

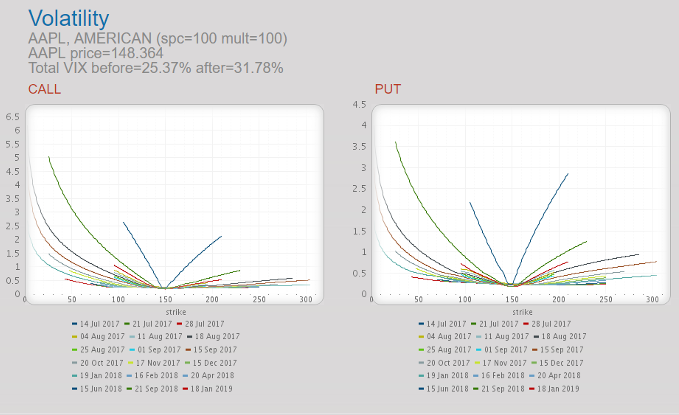

VIX-style Implied Volatility

Implied volatility is used by investors to estimate the volatility of the underlying asset expected by options traders. The implied volatility of a series or a chain is a VIX-like index calculated per the respective universe of options (see the methodology of VIX). Apart from the final index value for the option chain, dxFeed provides insights on the implied volatility of series that were chosen according to the VIX methodology for option chain volatility calculation.

Volatility Surface

Volatility Surface is a powerful tool, providing option traders with insight on computing the forward volatilities, which can be used for pricing of option products. The dxFeed methodology allows one to build volatility curves even for low liquidity markets, where option series do not have a whole set of strikes.