Overview

dxFeed Options Scanner is a powerful SaaS platform that enables real-time scanning of the entire options and equities universe using a wide variety of criteria.

dxFeed Options Scanner solves some of the financial industry’s most challenging questions:

- How to find the right investment instruments

- How to get real-time trading triggers

Why Options Scanner?

Greeks and IV calculation, VIX

and ATM IV and others

universe of US and European

options and equities

closest proximity to exchanges

architects consult on complex

solutions

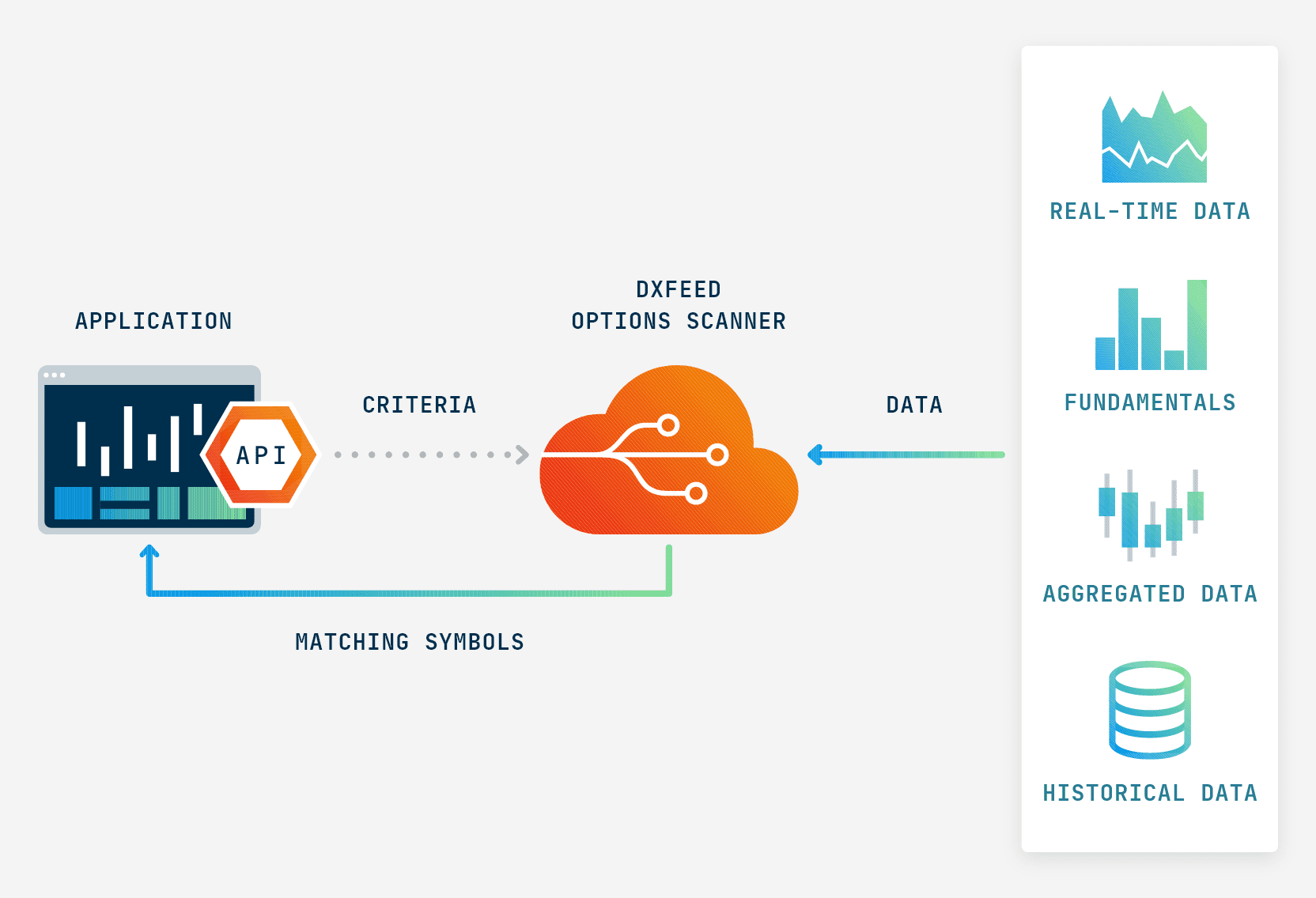

How dxFeed Options Scanner works

Highlights

Data available

Theoretical prices

Aggregations of options data on the underlying level

Options descriptive data

Greeks and implied volatility

Aggregated data

Historical indicators

Maturity curves on the underlying level

All data available for underlyings

Use case: option strategy based on IV to SV ratio

Problem

In modern financial markets it is becoming increasingly difficult to keep up with the flow of information. The right set of tools is often the key to understanding what’s important and what’s not. This is especially true in the case of option markets where the number of outstanding contracts is enormous.

Solution

Here we examine one possible scenario of options analysis using dxFeed Options Scanner.

The ratio of implied (IV) and statistical (SV) volatility of the underlying security measures the relation between the theoretical and the market price of the option. A high ratio indicates the option is overpriced (e.g, investors treat the asset as a hedge) and vice versa (e.g., insufficient liquidity).

If the ratio is sufficiently high, (e.g., greater than 1.3), it is a possible sign that option-selling strategies are viable. There’s a range of applicable approaches, such as selling the naked or covered option, or shorting the straddle (a combination of a call and put), to name a few. While the choice of a particular strategy is up to each trader’s style and risk preference, dxFeed Options Scanner allows them to quickly highlight cases for further analysis. We would also like to narrow our search down to the options near the money, with a strike price between 0.95 and 1.05 of the latest available price of the underlying security.